The Invisible Chains of High-Interest Debt

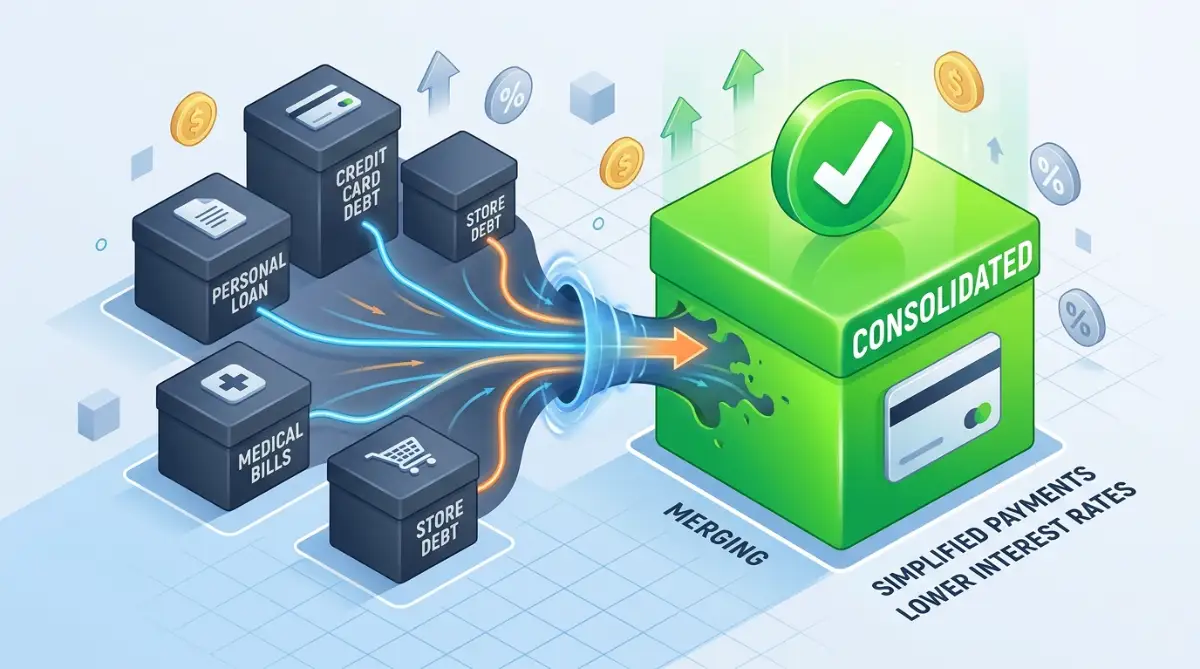

I know exactly how it feels. You wake up at 2 AM, and the first thing that hits you is the math. You are trying to remember if you paid the credit card bill that was due on the 15th. Then you remember there are three other cards, a personal loan, and a store bill waiting for you. The weight of these multiple payments feels like a heavy blanket that you can’t throw off. It is not just about the money; it is about the constant mental fog that debt creates in your daily life.

You are working hard every single day. But it feels like your paycheck is just a "guest" in your bank account. It arrives, stays for an hour, and then leaves to pay ten different lenders. Most of that money is just going toward interest, not even touching the actual balance. This is the reality for millions of people who feel trapped in a cycle that never seems to end.

Many people try to fix this, but they often hit a wall for these reasons:

- Traditional banks ask for a house or a car as security, which you might not have or don't want to risk.

- The "interest trap" keeps you small, where you only pay the minimum and the balance stays the same for years.

- Bad advice from the internet tells you to take "payday loans" which actually make the problem much worse.

- Confusing bank talk and hidden fees make people afraid to even ask for a better deal.

- The fear of rejection stops many from applying for a better loan that could actually save them money.

This struggle does more than just hurt your wallet. It slowly breaks down your mental peace and your confidence.

- You lose sleep and find it hard to focus at your job because the "debt monster" is always in your head.

- Your relationships with your family start to feel the heat as money becomes the main topic of every argument.

- You stop dreaming about the future because you are too busy just trying to survive the next thirty days.

- Your self-worth drops every time you have to say "no" to a fun dinner or a trip because of your bills.

- The constant anxiety makes it hard to be present for the people who actually matter in your life.

The truth is that the banking world can be cold. Most big banks want to play it safe. They want to see a deed to a house or a massive savings account before they trust you. If you don't have those things, you feel like a second-class citizen in the financial world. It feels like the system is rigged to help the people who already have money, while you are left to drown in high-interest cards.

But things are changing. There is a path for people who have a steady income but no physical assets to "pledge." This is where no-collateral bank loans come in. These loans are based on your character and your ability to pay, not on your house or your car. When used for debt consolidation, they act like a "reset button" for your financial life. You take one big loan at a lower rate, pay off all the small "vampire" debts, and start breathing again.

A Clear Roadmap to Reclaim Your Financial Future

Reclaiming your life from debt is a journey. It requires a plan that is both smart and simple. Since you are not using collateral, the bank is going to look at you very closely. You need to present yourself as a "safe bet." Here are the first three steps to prepare your life for a successful consolidation loan.

Step 1: Mapping Your Financial World

Before you talk to a bank, you must be the master of your own data. Most people avoid looking at their total debt because it is scary. I want you to do the opposite. Sit down with a piece of paper and list every single debt you have. Write down the total balance, the monthly payment, and most importantly, the Interest Rate (APR).

When you see that one card is charging you 25% and another is 29%, you will feel a new kind of energy. This is not fear; it is a "healthy anger" at the money you are wasting. This list is your map. You now know exactly how much you need to borrow to wipe the slate clean.

Knowing your total number allows you to speak to a banker with absolute confidence. Instead of saying "I think I need some money," you can say "I need exactly $15,000 to consolidate these specific debts." Bankers love this. It shows you are organized, serious, and in control. This level of preparation is your "virtual collateral."

Step 2: Strengthening Your Borrower Identity

Since the bank has no house to take if things go wrong, they look at your reputation. This is your credit score and your income history. You don't need a perfect score, but you do need a "clean" one. Spend thirty days before applying to make sure there are no errors on your credit report. Small mistakes can often drop your score by 50 points for no reason.

Another trick is to look at your "Credit Utilization." If your cards are all maxed out, you look risky. Even if you can't pay them off yet, try to pay a little bit more on the smallest one to show some "white space" on your credit lines. It shows the bank's computer that you are not desperate, but you are strategic.

Your job history is also part of your identity. If you have been at the same job for a year or more, that is a huge win. It tells the bank that your income is reliable and steady. They aren't just lending to a name; they are lending to a steady paycheck. If you can show them that you are a stable person, they will be much more likely to ignore a slightly lower credit score.

Step 3: Hunting for the Perfect Lending Partner

Not all banks are created equal. If you go to a massive national bank, you might just be a number in their machine. They have very strict rules and often don't have time for your "story." I often suggest looking at Regional Banks or Local Credit Unions. These institutions are more "human." They want to help the people in their own community.

Credit Unions, in particular, are non-profit. Their goal is to serve their members, not to make billions for shareholders. They often have lower interest rates for unsecured loans because their "mission" is to help you improve your life. Walk into a local branch and ask to speak with a loan officer. Explain that you want to be more responsible by consolidating your debts into one manageable payment.

Also, look at modern "Fintech" online lenders. These companies use smart technology to look at more than just a credit score. They might look at your education or your job title to see your future potential. Many of them offer "pre-qualification" with a "soft credit pull." This means you can see your rate without hurting your credit score. It is like "window shopping" for a loan, and it is a very smart way to find the best deal without any risk.

The Power of the Single Payment

Why is a single payment so life-changing? It is about mental bandwidth. When you have five different due dates, your brain is always "on." You are always checking the calendar. This creates a state of low-level stress that never goes away. When you consolidate, you have one date and one amount.

This simplicity allows you to focus on your life again. You can spend that mental energy on your job, your hobbies, or your kids. Plus, because the interest rate is lower, more of your money goes toward the "principal" debt. You will see your balance drop every single month. This creates a positive feedback loop. When you see the debt disappearing, you feel motivated to keep going.

Think of debt consolidation like a bridge. On one side, you have the chaotic, high-interest land of multiple bills. On the other side, you have the calm land of financial freedom. The no-collateral loan is the bridge that takes you across. You don't have to risk your house to cross that bridge. You just need a solid plan and the right partner to help you take the first step.

Understanding the "APR" Advantage

The biggest secret to winning this game is the APR (Annual Percentage Rate). Most credit cards have an APR between 20% and 30%. A good no-collateral bank loan might have an APR between 8% and 15%. This is a massive difference.

Imagine you owe $10,000. At 25% interest, you are paying over $2,000 a year just in interest! That is money you are throwing into the trash. If you consolidate that to a 10% loan, you instantly save $1,500 a year. That is $125 extra in your pocket every single month. That is money for groceries, gas, or just a little bit of peace of mind. This math is why consolidation is the smartest move you can make when you feel stuck.

Why Organization is Your Secret Weapon

Banks love borrowers who are organized. When you apply for an unsecured loan, have your papers ready. This means your last three months of pay stubs, your tax returns, and a list of the debts you want to pay off. When you provide these in five minutes instead of five days, the banker thinks "This person is ready."

Disorganized people look like a risk. Organized people look like a professional partner. By having your "Trust Folder" ready, you are proving that you are the kind of person who handles money with care. This alone can move your application from the "maybe" pile to the "approved" pile. You are making it easy for the bank to say "Yes" to you.

Preparing for the "New Normal"

Debt consolidation is a "reset," but you must be ready for the "new normal." Once you get the loan and pay off your cards, your cards will have a zero balance. This is a dangerous moment. Many people feel "rich" and start spending on the cards again.

You must be stronger than that. Use this loan as a fresh start. Hide the cards or put them in a drawer. Focus only on the single loan payment. You are not just changing your loan; you are changing your habits. This is how you ensure that once you get out of debt, you stay out forever. You are building a life based on freedom, not on interest payments.

By following these three steps—auditing your debt, strengthening your identity, and choosing the right lender—you are setting yourself up for a massive win. You don't need a house to pledge. You just need the courage to face your numbers and the wisdom to use the tools available to you. The path to a stress-free life is open. It is time to take that first step across the bridge.

Using Modern Strategies to Lock in the Best Terms

Now that you have your documents and credit score ready, it is time to look at the expert secrets. These are the small moves that save you thousands of dollars in interest. Most people just take the first offer they see. I want you to be much smarter than that.

The Hidden Benefit of Automatic Payments

One of the best-kept secrets in banking is the Autopay Discount. Most lenders want to know for sure that they will get their money on time. To encourage this, they often offer a 0.25% to 0.50% reduction in your interest rate.

This might sound small, but on a $20,000 loan, it adds up over time. It is like getting a small "thank you" gift from the bank every single month. Plus, it removes the human error of forgetting a due date.

When you set up automatic payments, you are proving to the bank's system that you are a high-trust borrower. This builds a bridge of reliability that helps your credit score grow even faster. It is the easiest way to lower your costs without doing any extra work.

Comparison Shopping Without Damaging Your Score

Many people are afraid to look at different banks because they think it will hurt their credit. But in the modern world, we have Soft Credit Pulls. This is a way for a bank to give you an "estimated" rate without a formal mark on your record.

I always suggest that you check at least three different lenders. You might find that a credit union in your town has a much better deal than a big online bank. Or, you might find that one lender has no hidden fees.

Think of it like buying a car. You would never buy the first car you see at the first dealership. You look around to find the best price and the best features. Your debt consolidation loan deserves that same level of care and research.

How to Maintain Your New Financial Freedom

Getting the loan is a massive win, but keeping that freedom is a long-term game. You need a simple system to make sure you never end up back in the debt cycle. Here is a professional guideline you can follow to stay safe.

- Build a Starter Emergency Fund: While you are paying off your new loan, try to save just $500 or $1,000. This is your "shield" against new debt. If your car breaks, you use this cash instead of a credit card.

- The 24-Hour Rule for Spending: If you want to buy something that isn't a basic need, wait one full day. Often, the "urge" to buy goes away after a good night's sleep. This keeps your bank account healthy and strong.

- Track Your Progress Monthly: Use a simple app or a notebook to watch your loan balance drop. Seeing the number get smaller is very addictive. It gives you a mental boost that keeps you focused on your goal.

- Talk About Money Honestly: If you have a partner, sit down once a month and look at the numbers together. When you are both on the same team, you move twice as fast toward your dreams.

This guideline is about more than just numbers; it is about peace of mind. It allows you to be the boss of your money instead of your money being the boss of you. By following these steps, you are ensuring that your debt consolidation loan is a permanent fix, not a temporary patch.

Avoiding the Traps That Keep People in Debt

Even with a perfect plan, there are "hidden holes" that can sink your progress. I have seen many people get a consolidation loan and then find themselves in even more debt a year later. I want to make sure that never happens to you.

The "Double Debt" Danger

This is the most common mistake. People get a loan, pay off their credit cards, and suddenly see zero balances on their card statements. They feel "rich" and start using those cards again for dinner, clothes, or trips.

Suddenly, they have the new loan payment plus new credit card bills. This is a financial nightmare. To avoid this, you must hide your cards or even cut them up until the loan is halfway paid off. Use this loan as a chance to break the habit of using credit for daily life.

Ignoring the Sneaky Origination Fees

Some lenders brag about a low interest rate but hide a big fee in the fine print. An Origination Fee is a charge taken out of the loan before you even get the money. If you borrow $10,000 and the fee is 5%, you only get $9,500.

However, you still have to pay interest on the full $10,000. Always ask the lender, "What is the total amount that will hit my bank account?" If the fees are too high, it might be better to choose a loan with a slightly higher interest rate but no fees. Always do the math on the total cost.

Stretching the Loan Term Too Long

It is very tempting to pick a 5-year loan because the monthly payment is small. But a longer loan means you will pay much more in interest over the total life of the debt. You might pay off your cards, but you end up staying in debt for years longer than necessary.

Try to pick the shortest term that you can realistically afford. If you can pay an extra $50 a month, do it. This small move can shave months off your loan and keep thousands of dollars in your pocket. Be aggressive with your repayment so you can be free as soon as possible.

Falling for "No Credit Check" Scams

When you are looking for no-collateral loans, you will see many ads for "Guaranteed Approval." Be very careful. These are often predatory lenders who charge 300% or 400% interest.

A real bank or a trusted online lender will always check your history in some way. They want to make sure you can actually afford the loan. If a deal looks too good to be true, it usually is a trap designed to keep you in debt forever. Stick to well-known banks and credit unions.

Missing a Single Payment on the New Loan

Your new consolidation loan is your "fresh start." If you miss a payment on this loan, your credit score will drop very fast. It tells the banking world that you are still struggling even after getting help.

This is why the automatic payment secret I mentioned earlier is so important. You want your payment to be like a clock. It should happen every month without you even thinking about it. This builds a perfect history that will make your next loan or mortgage much cheaper.

Your New Chapter of Financial Clarity Starts Today

You have done the hard work of learning the system. You know how to audit your debt, how to find the right lender, and how to avoid the traps. You are no longer just "hoping" for a better life; you are actively building one with smart choices.

Think about how it will feel when you have just one simple payment every month. Imagine the relief of seeing those high-interest credit cards closed and gone. You are taking back control of your time, your energy, and your future. This is a massive win for you and your family.

I want to encourage you to take the first step right now. Don't wait for a "perfect" moment because it will never come. Open your bank app, look at your highest interest card, and write down that APR. That number is your motivation to find a better way.

You are a capable, smart person who deserves to live a life free from debt stress. You have the map, you have the secrets, and now you have the plan. Go out there and reclaim your financial peace today. Your future self is already thanking you for the brave choice you are making right now.